While the broader market has struggled with the S&P 500 down 5.3% since October 2024, Fastenal has surged ahead as its stock price has climbed by 6% to $81.29 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Fastenal, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We’re glad investors have benefited from the price increase, but we're cautious about Fastenal. Here are three reasons why we avoid FAST and a stock we'd rather own.

Why Is Fastenal Not Exciting?

Founded in 1967, Fastenal (NASDAQ:FAST) provides industrial and construction supplies, including fasteners, tools, safety products, and many other product categories to businesses globally.

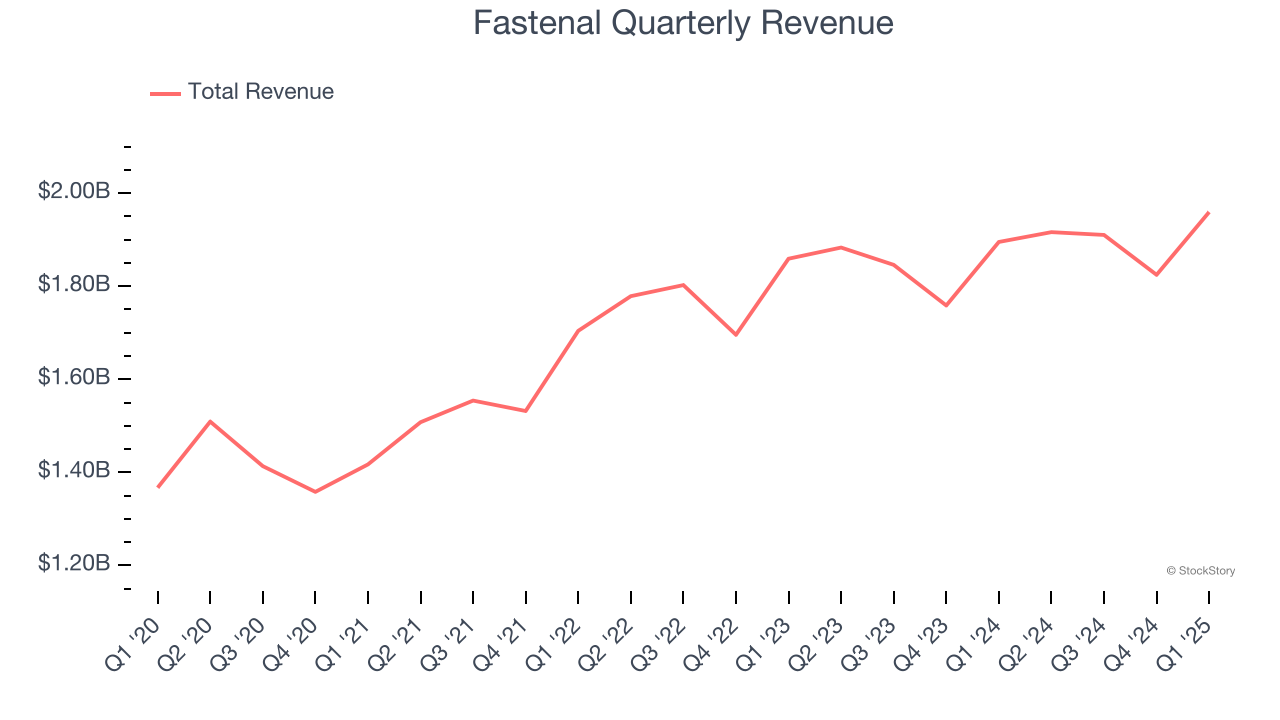

1. Long-Term Revenue Growth Disappoints

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Fastenal grew its sales at a mediocre 7.1% compounded annual growth rate. This fell short of our benchmark for the industrials sector.

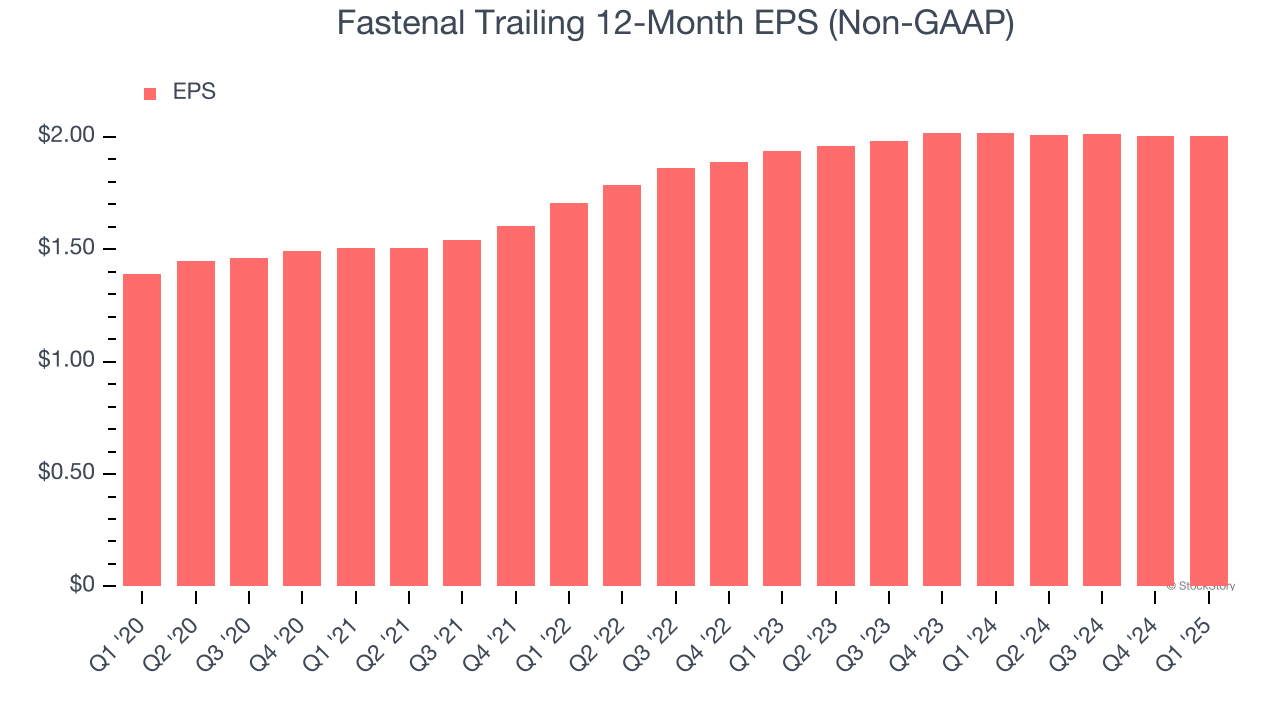

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Fastenal’s unimpressive 7.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

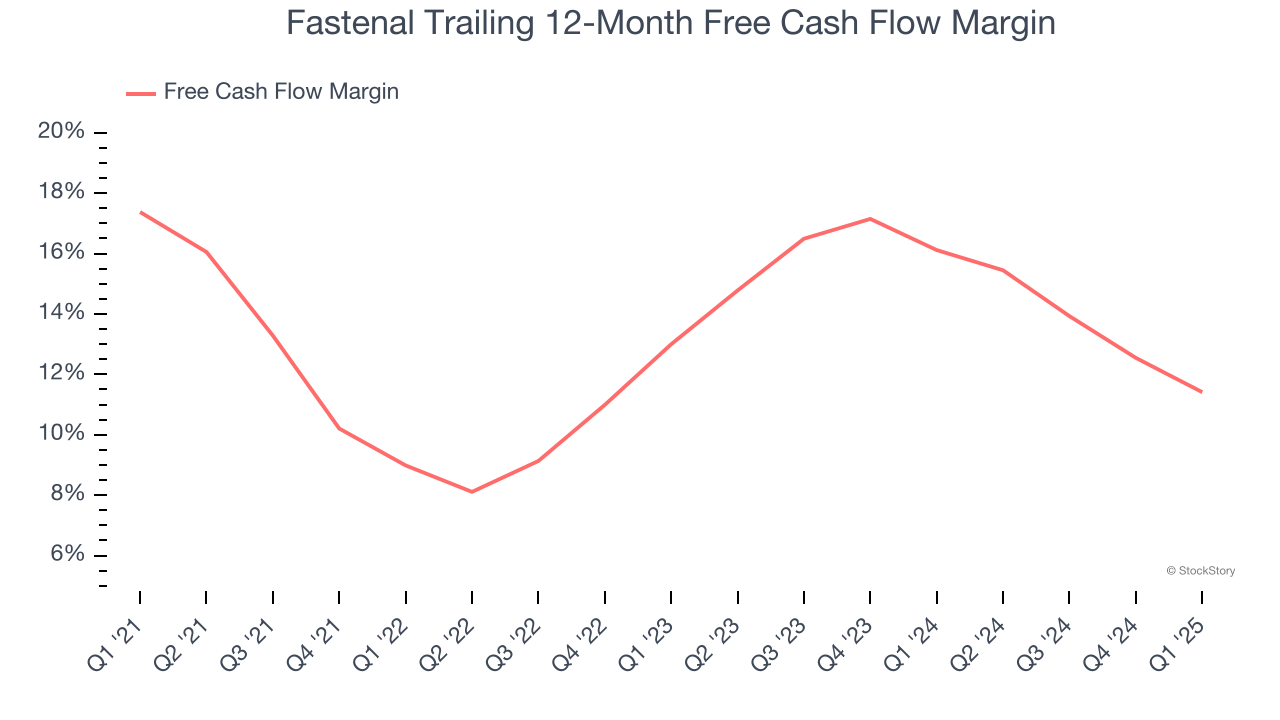

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Fastenal’s margin dropped by 6 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Fastenal’s free cash flow margin for the trailing 12 months was 11.4%.

Final Judgment

Fastenal isn’t a terrible business, but it doesn’t pass our quality test. With its shares topping the market in recent months, the stock trades at 36.7× forward price-to-earnings (or $81.29 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than Fastenal

Market indices reached historic highs following Donald Trump’s presidential victory in November 2024, but the outlook for 2025 is clouded by new trade policies that could impact business confidence and growth.

While this has caused many investors to adopt a "fearful" wait-and-see approach, we’re leaning into our best ideas that can grow regardless of the political or macroeconomic climate. Take advantage of Mr. Market by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.