EPAM has gotten torched over the last six months - since December 2024, its stock price has dropped 32.9% to $163.49 per share. This might have investors contemplating their next move.

Is now the time to buy EPAM, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is EPAM Not Exciting?

Even though the stock has become cheaper, we're swiping left on EPAM for now. Here are three reasons why you should be careful with EPAM and a stock we'd rather own.

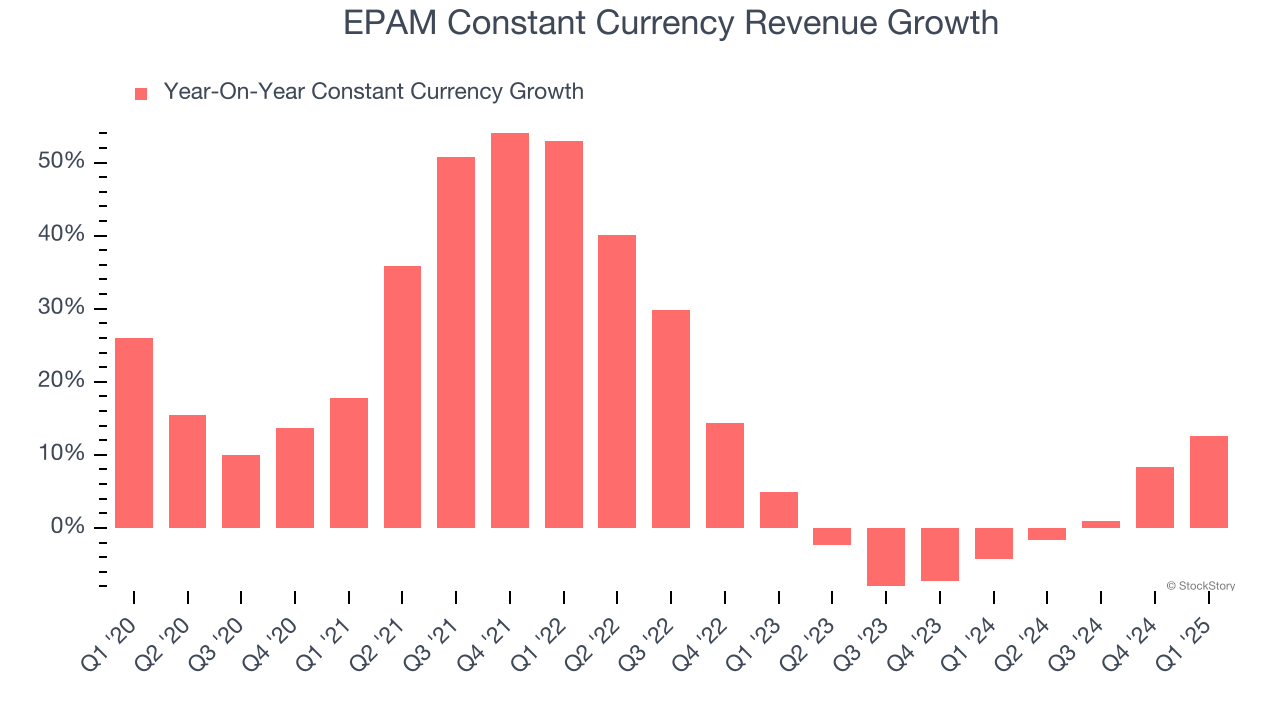

1. Constant Currency Revenue Hits a Standstill

In addition to reported revenue, constant currency revenue is a useful data point for analyzing IT Services & Consulting companies. This metric excludes currency movements, which are outside of EPAM’s control and are not indicative of underlying demand.

Over the last two years, EPAM failed to grow its constant currency revenue. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests EPAM might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

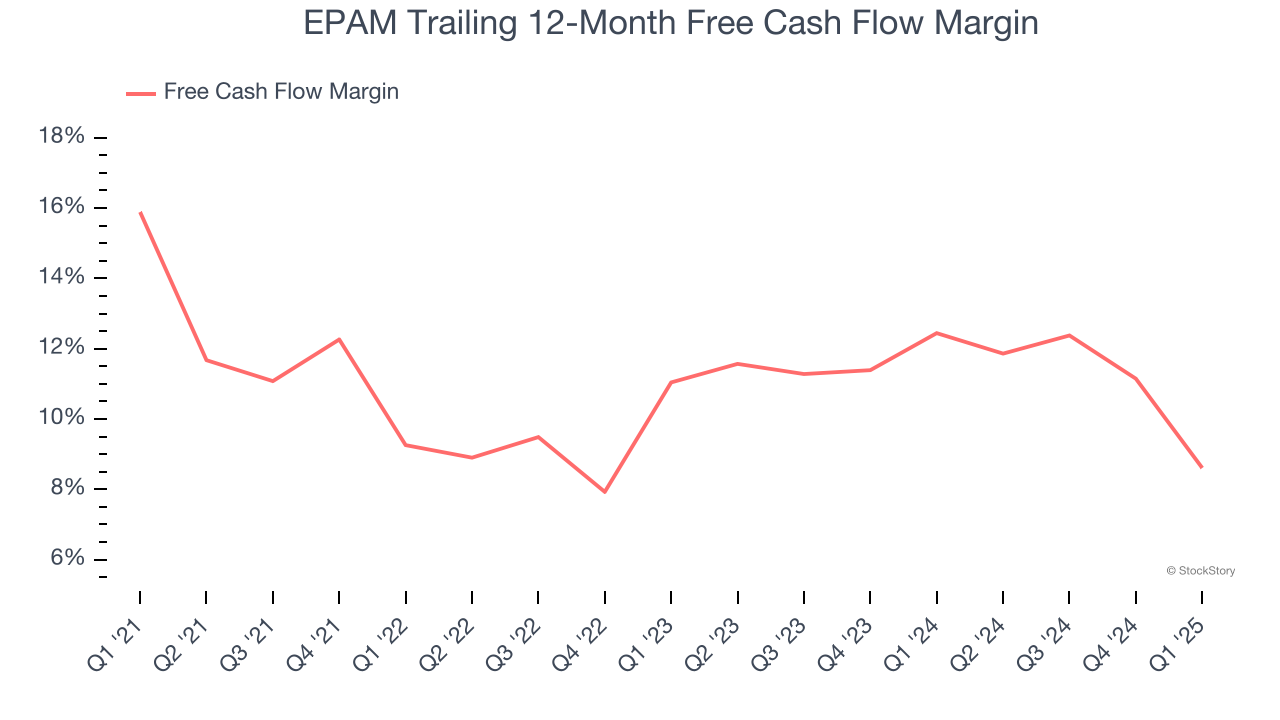

2. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, EPAM’s margin dropped by 7.3 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. EPAM’s free cash flow margin for the trailing 12 months was 8.6%.

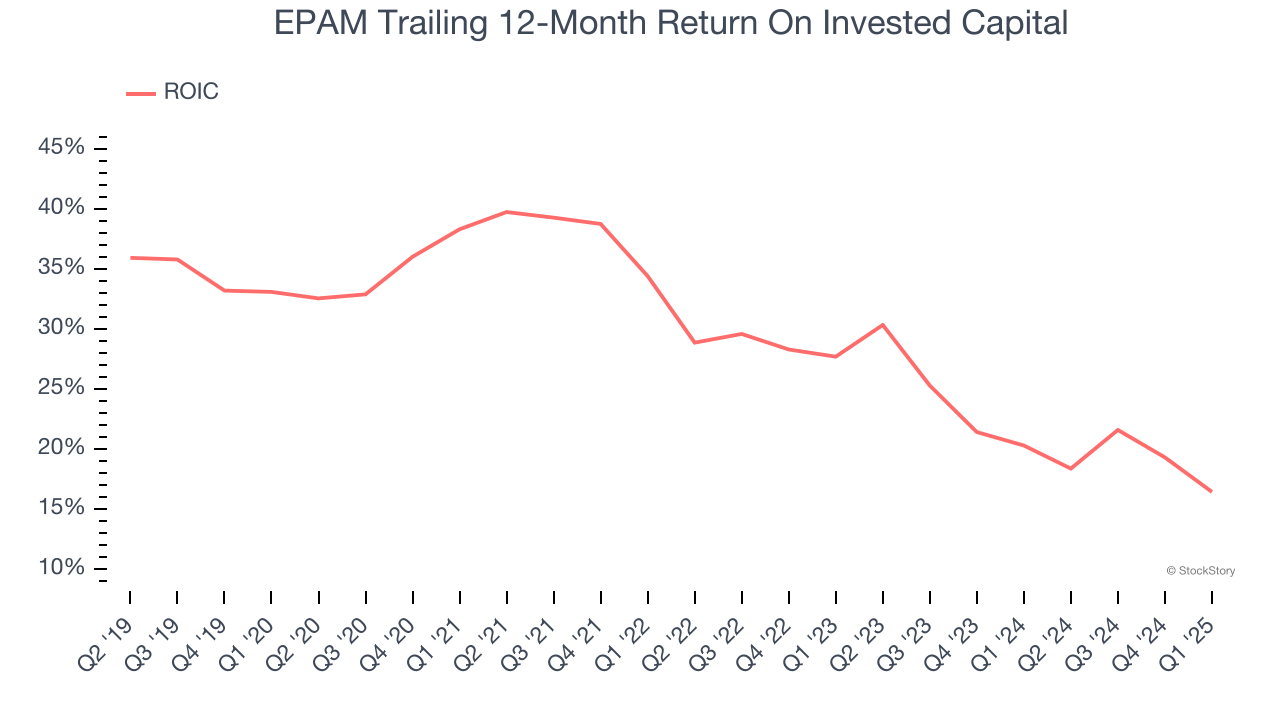

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, EPAM’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

EPAM’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 15× forward P/E (or $163.49 per share). Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.